Briefing note

Inflation Update

06 Sep 2022

Key messages of this briefing note:

- Risks to inflation remain firmly skewed to upside as energy prices continue to rise

- Expect falling real wages and rising costs to weigh heavily on the growth outlook

- Central banks likely to continue raising rates in near-term, despite economic weakness

- Impact on schemes will depend upon the degree of inflation linkage in liabilities, level of interest- and inflation-rate hedging, and the mix of assets.

Energy prices are intensifying near-term inflation pressures

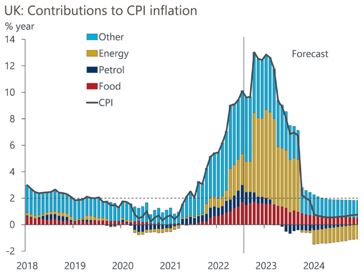

Further upside surprises in inflation and ongoing increases in energy prices are creating a corrosive effect on real incomes, with real average pay suffering the biggest fall on record in July. Headline CPI inflation reached double digits in July, rising to 10.1% from 9.4% in June. Inflation has continued to exceed both consensus and the Bank of England’s (BoE’s) forecasts. The biggest driver of July’s increase in inflation was a sizeable 2.3% month-on-month increase in food prices, but core CPI also increased, rising to 6.2% from 5.8%.

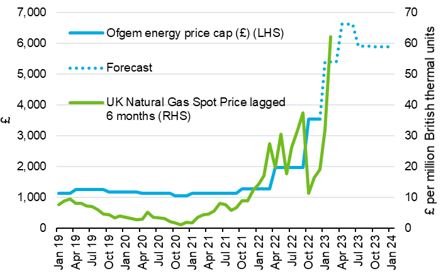

With Ofgem confirming the energy price cap will increase by 80% from October, UK headline CPI is likely to reach 13% year-on-year that month (Chart 1). As gas futures prices have continued to rise, further large increases in the cap look likely in early 2023 (Chart 2). We expect energy prices and inflation to rise further in the near-term and expect continued downgrades to growth forecasts as consumer’s real pay falls at a record pace and businesses struggle with rising costs. While the Office for National Statistics (ONS) has stated that the government support on energy prices announced to date will not influence their calculation of inflation, any potential future government intervention, and how this may be treated by the ONS, creates an additional layer of uncertainty around inflation.

Chart 1: CPI inflation likely to reach 13% in the autumn

Chart 2: Gas prices and Ofgem price cap

While the risks to headline inflation remain skewed to the upside, core inflation, which excludes more volatile elements such as food and fuels prices, had been showing some signs of weakening prior to July’s release. July’s year-on-year core inflation reading was pushed up by an unusually weak reading in July 2021, but there remain signs that underlying inflationary pressures may be moderating. Growth in factory gate prices slowed for the first time since December 2021, recent falls in the price of oil and agricultural commodities suggest that fuel and food price inflation may be close to peaking, and global shipping costs have dropped. Also, while a sharp fall in real wages is painful for consumers, it does at least suggest that inflation has not yet become fully entrenched.

Bank of England response

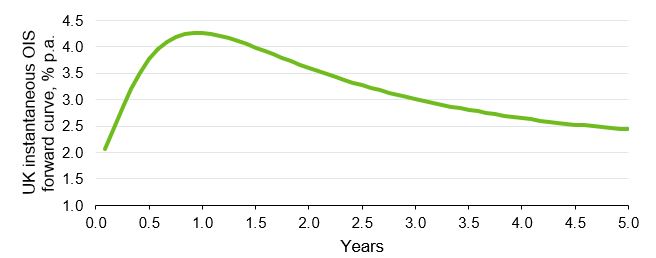

While central banks typically try to look through supply-side shocks and focus on core inflation, we expect the BoE to remain firmly in tightening mode in the near-term, and this looks at least fairly reflected in market pricing (Chart 3). The BoE’s August Monetary Policy Committee meeting minutes showed the BoE has shifted from setting policy according to their central forecast to targeting the risk that high inflation becomes embedded in business and consumer inflation expectations. This is evidenced by the MPC voting to accelerate the pace of tightening in the near-term, despite their central forecasts showing a significant inflation undershoot over the forecast horizon. Indeed, the markets anticipate that the BoE will start cutting rates in 2023 as growth, and presumably inflation, falters.

Chart 3: Markets expect the BoE to raise interest rates sharply in the near-term before cutting in H2 2023

Impact on investment returns

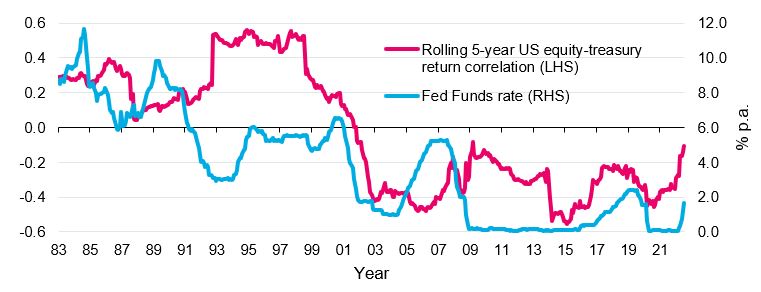

Historically, during periods of moderately positive inflation, bond and equity returns have tended to be negatively correlated (Chart 4). When interest rates are rising to combat high inflation, bond and equity prices have tended to fall at the same time, as has been the case this year. Real assets, such as property and commodities, in contrast, have been some of the very few sources of positive returns in 2022.

Chart 4: Since the Federal Reserve started targeting inflation, US equities and US Treasury bonds have, on average, been negatively correlated.

The withdrawal of monetary policy accommodation in the major advanced economies has led to asset price deflation. We believe much of the price decline in equity markets year-to-date, reflects a de-rating of valuation multiples due to rising real yields. Valuations are now far less stretched than at the start of the year, but the impact on economic activity and corporate earnings from high inflation and tighter financial conditions may yet to be fully reflected in market prices.

Perhaps the only silver lining is that forward-looking nominal returns on bonds, credit, and equity have potentially improved since the beginning of the year, when low yields, tight credit spreads, and high equity price to earnings ratios, pointed to subdued medium-to-long-term returns from the major asset classes.

Impact on sterling

Expectations of higher interest rates tend to cause a currency to strengthen relative to its peers. However, other central banks have also been raising interest rates in 2022 and, as Chart 3 above illustrates, markets do not believe the near-term BoE rate hikes priced are sustainable. Consensus forecasts are that the UK will face one of the highest inflation rates over 2022 and 2023, and also one of the lowest real growth rates, among developed economies. Currency markets have focussed on medium-term economic weakness, rather than near-term rate rises. Sterling has fallen as a result, down close to 13% against the dollar, though only down c.2.5% in trade-weighted terms as the dollar has also strengthened against most other major currencies year-to-date. Sterling weakness has boosted global equity returns to unhedged sterling-based investors and sterling now looks historically cheap versus the dollar, but it is difficult to see a catalyst that may reverse its fortunes in the near-term.

Impact on pension liabilities

For pension schemes with uncapped pension increases linked to inflation, the nominal value of pension payments will increase in the short-term, putting cashflows under strain, but the rise in longer-term yields this year will have actually improved long-term funding levels in many cases. The exact impact on liabilities will, of course, vary from scheme to scheme, and will depend upon the degree of inflation-linkage in benefits and the level of interest- and inflation-rate hedging in place. Schemes with shorter duration, and floating-rate, fixed income assets will have seen smaller falls in the value of their assets year-to-date. As will those with larger exposures to real assets, such as property and commodities.

If you have any questions, please get in touch.

0 comments on this post