In the immediate response to the COVID-19 pandemic, we have seen a whole flurry of activity across the UK life insurance sector. From initiating business continuity plans, reviewing underwriting processes, offering premium holidays, through to recalculating solvency positions (some daily, some weekly) and amending hedging strategies, plus much more. It has certainly been a busy few weeks for insurers.

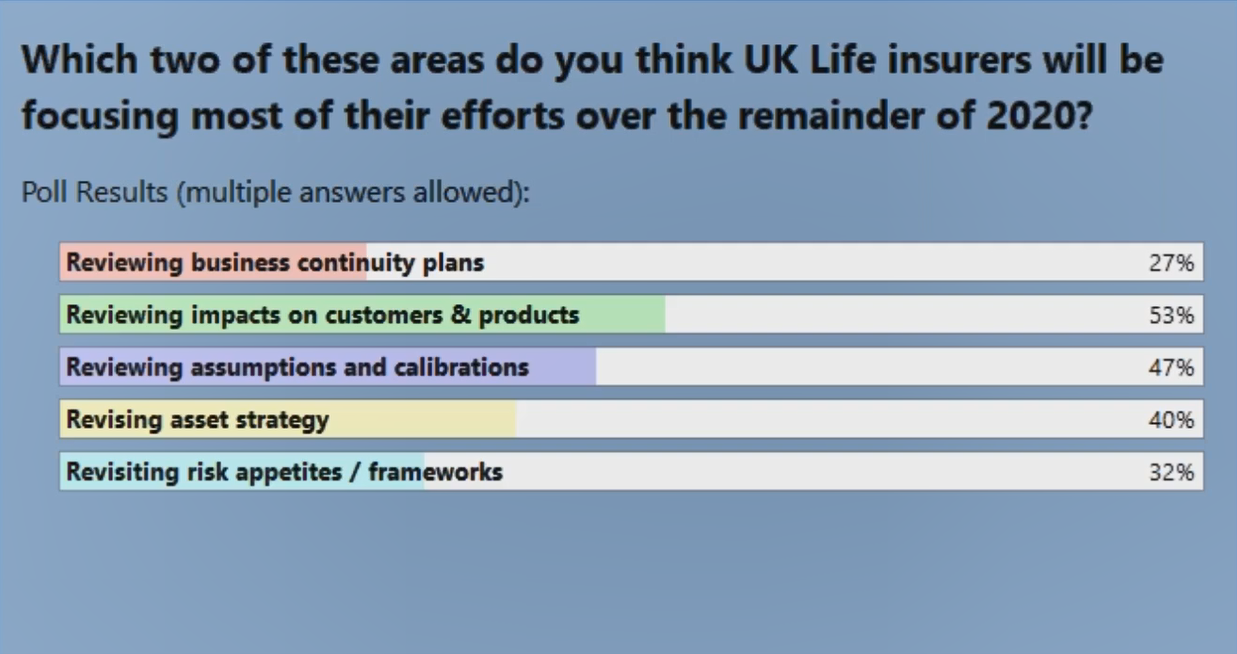

But what next? What will the next few months hold, and where do insurers plan to focus their attention? A recent Hymans Robertson poll of insurance executives (a sample of 219 on 23 April 2020) highlights the areas they expect insurers will be focussing on.

The results show they expected insurers to spend relatively more effort over the remainder of 2020 on reviewing the impacts on customers and products with 53% agreeing. Next were reviewing assumptions and calibrations (at 47%), closely followed by revising their asset strategy (40%) and revisiting risk appetites and frameworks (32%). In the rest of the blog we consider some of the specific areas insurers should focus on within these areas of focus.

Impact on customers and products

It’s no doubt the pandemic has and will have a massive impact on customers, particularly as the effects of the lockdown begin to work their way through the economy. Some of the areas we expect insurers to focus on in respect of customers are:

Understanding lapses: There is some concern we might see an increase in lapses due to the economic consequences of lockdown flowing through to lower affordability amongst customers. However, we know some providers are offering premium holidays so that will help offset this impact. We also know that protection insurance is thought to be one of the last items of spending customers will stop, particularly in the current situation. So it could be a mixed picture for lapses, and insurers will need to carefully consider the impact of any interim measures they put in place, and whether their customers are more or less exposed to the economic fallout than average.

Indirect COVID-19 claims: Besides the direct claims from COVID-19, there will undoubtedly be indirect claims arising from the lockdown. For example, the effects of isolation in lockdown or increasing unemployment is expected to impact mental health. We know many people are staying away from A&E and GPs too. Then there is the impact of deferring tens of thousands of elective surgeries/treatments for other conditions. What problems will this store up? Insurers will need to carefully consider the potential impact on claims. Also insurers should consider what part they can play in encouraging customers to use additional digital services to seek medical advice and make sure we are not storing up too many problems for the future.

Access to insurance: There is a lot of concern that we will see vulnerable customers finding if more difficult to access insurance because of delays in underwriting. More caution amongst providers in assessing those with underlying conditions and more at risk of COVID-19 complications. So insurers should consider how they are minimising the impact of any changes on vulnerable customers.

Reviewing assumptions and calibrations

Another area of high focus will be reviewing assumptions and calibrations, perhaps as the industry gets ready to update its year end, or even half year reporting:

Lapse assumptions: Given the lapse impacts noted above, long-term lapse assumptions will need careful consideration at a sub-product level to ensure appropriate long-term assumptions are set and we see short-term provisions implemented to allow for uncertainty in the short term.

Longevity, mortality and morbidity assumptions: Short-term provisions may also be appropriate for these assumptions given the uncertainty of the short-term impact of COVID-19 on claims and the uncertainty of the impact on mortality improvements. The differences in assumptions by socioeconomic group is likely to also become an area of focus for insurers and their auditors.

Internal model calibrations: Insurers will need to use the new information gathered during this crisis to validate their internal models. Market risks, in particular, will need to be considered to assess whether calibrations are currently strong enough given the second market crisis in the past 15 years. Although we aren’t currently seeing claims hitting the tails of typical insurance risk calibrations, these will also need to be monitored closely – in particular any allowance for “uncertainty” within calibrations. The current conditions also gives an opportunity to validate all correlation assumptions, particularly between catastrophe risks and market risks.

Revisiting asset strategies and risk frameworks

Reviewing asset strategies and risk frameworks featured as lower priorities in our poll. Perhaps insurers feel existing strategies should be resilient and it’s more a case of evolving rather than replacing existing ones. However, we still anticipate that firms will be considering their asset strategies in areas such as:

Asset valuation uncertainty: the current market environment creates uncertainty around the valuation of certain assets, including real estate. Valuations typically take account of achievable rental income, as well as transaction pricing. The current situation – with businesses and the market not functioning as normal – makes these indicators harder to pin down. Where such assets provide the security for lending made by insurers, there may further impacts on internal ratings and, therefore, on the matching adjustment and solvency capital requirements.

Investing new business premiums: when deciding where to invest new business premiums, firms may need to reconsider the balance between public and private assets given that the relative spreads available on these assets and potential changes in risk appetite. Firms may consider targeting sectors which are less affected by the current situation, or identify opportunities which appear more attractive at the moment. Firms will also need to consider how much of any spread widening they should reflect in pricing of new business. This will be particularly relevant for annuity firms that operate under the matching adjustment, where the fundamental spread (allowance for defaults and downgrades) is relatively insensitive to market movements.

De-risking of investment portfolios: insurers typically hold well-diversified portfolios and are accustomed to managing against default and downgrade risk. Nevertheless, we anticipate some de-risking activity will take place, particularly where firms have concerns around a ‘second wave’. We have already seen some with-profit funds de-risk from equities into less risky assets due to internal triggers being hit by the current equity levels.

Reviewing business continuity plans

The area expected to receive the least focus is business continuity plans. Although these plans would have already been put into action, some work may still be required to adapt them, taking into account learnings from how the crisis has played out in reality.

Regardless of which areas life insurers do focus on most over the next few months, one thing is certain, the next few months will be just as busy for life insurers as the last few weeks.

If you would like to discuss anything mentioned in this blog, please do get in touch.

0 comments on this post