COVID-19 is impacting customers in different ways, from their health through to their finances, and driving changes in customer behaviour and priorities. In our second Hot Topics in Life Insurance webinar, we considered the potential implications of COVID-19 for life insurer products and customers. We looked at what providers could do to respond to customers' needs and changes in their behaviour, how product terms could evolve, and what communications may be required.

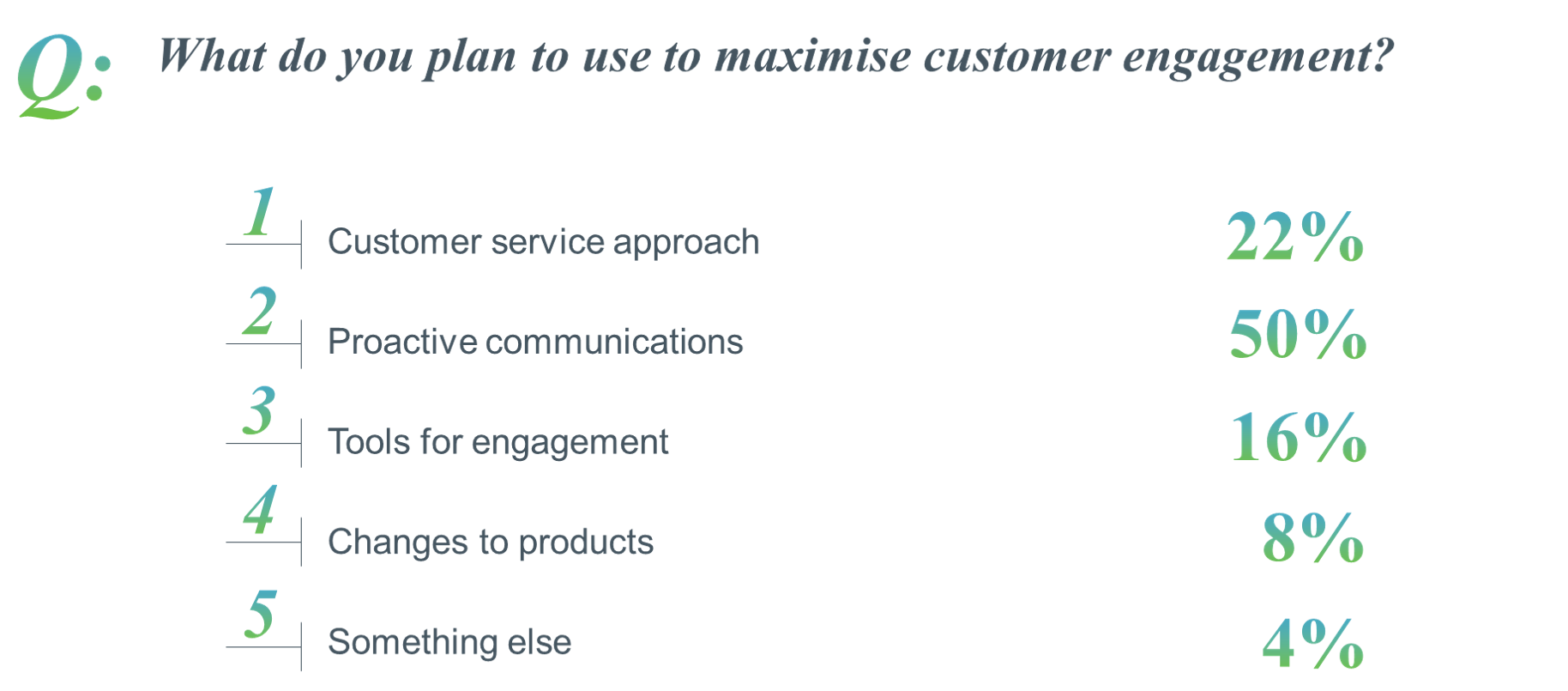

Our poll showed that proactive communications were considered the most important way to maximise customer engagement at this time with 50% planning to use this approach most in future. Providers also thought their customer service approach and tools were other meaningful ways to engage with customers, with 22% and 16% agreeing respectively.

How can insurers engage customers through proactive communications? We explore some of the ways relevant to the protection and retirement markets.

Proactive communications for protection

When it comes to protection insurance, many providers have responded very quickly to COVID-19, by making significant changes to their servicing processes. However, sometimes these changes, such as encouraging customers to go online rather than calling, have not been communicated clearly to customers, and this has meant it’s become more difficult for them to get access to products and services, particularly when the online journey is not easy to navigate or has not been updated to reflect the latest changes. So transparency on any product or service changes is really important.

By proactively communicating with customers, insurers can also take the opportunity to remind them of the cover they have in place. With COVID-19 preventing many people from seeking timely medical assistance, it means some customers are seeing an unnecessary deterioration in their health. So products like Critical Illness and Income Protection could provide more value than ever. Explaining what they are covered for, and how they can claim, could also help build trust amongst customers who can otherwise believe insurers are reluctant to pay valid claims.

For potential new customers who are not offered terms, can insurers also do more to support them and signpost other solutions? Putting customers’ needs first and supporting them in this way will be an important tool in widening access to insurance.

Proactive communications for retirement

When it comes to customers and their retirement savings we need to ensure we help them, reassure them and deliver good outcomes by helping them avoid poor decisions.

The reality is to do this reactively in a time of relative crisis, which is really hard. What communication can you send and how can you frame it such that you give the customer the right guidance (not advice), and stay within your own internal risk boundaries? “Don’t worry, markets always bounce back, everything is definitely going to be fine” is not an option.

However, it is possible to do this if you have already established a communication framework that concentrates on final outcomes. If this has been the customers main frame of reference from day one of engaging with you then it becomes much easier. You can do this if you have an outcomes based communication framework, as opposed to a pot size and investment risk as measured by volatility model, the more traditional approach.

From our experience of working with clients to implement retirement planning tools, there are two key factors to maximising engagement:

Present the actual impact of current falls in the light of what it has done to their long-term goals, as opposed to just looking at short term pot movement.

Provide guidance on the steps that customers can take in light of the market changes and their circumstances, including helping them understand the impact of a pension contribution holiday and how to get back on track.

How can we make it better?

In summary, providers should consider the following ways to make the most of the communications and engage customers:

Prepare people – we can’t predict the causes, but we do know that crashes will happen. What sort of communication framework can we adopt today to make it easier to help people when the next one happens?

Provide context – help people set goals and then measure outcomes, so they look at events with an understanding of the long term when it is a long term product.

Help people – you can gain so much customer trust and loyalty if you do it well in times of stress, and make financial services work even better for people at the same time.

If you would like to discuss further how you can engage your clients using proactive communications, utilising market leading customer tools or by developing your products, please get in touch with one of our team.

0 comments on this post